Congo’s Gecamines offers $1 million to block Chinese deal with Chemaf

Akobo Minerals opens Ethiopia’s Segele gold mine

Adani’s Australian coal unit faces human rights complaint

Panama’s President blames previous gov’t for First Quantum mine crisis

Panama’s President José Raúl Mulino has strongly condemned the previous government for its mismanagement of the crisis surrounding First Quantum Minerals’ (TSX: FM) $6.5 billion Cobre Panama copper mine.

The operation, First Quantum’s flagship mine, was shut down a year ago following a Supreme Court ruling that declared its concession contract unconstitutional.

Mulino attributed the closure to widespread public dissatisfaction with former President Laurentino Cortizo’s administration.

“The mine paid the price for accumulated national discontent, under a government with only 25% popularity and overwhelming public rejection,” stated Mulino, who took office in July, according to BNamericas. “They couldn’t manage such a critical issue, let alone in the manner they attempted.”

The decision to invalidate the mine’s permit followed mounting protests. Critics accused the Cortizo government of failing to address long standing legal and environmental concerns tied to the project, which accounted for nearly 5% of Panama’s GDP.

Mulino, now tasked with resolving the fallout, has vowed to take a more transparent approach, promising a comprehensive audit of the mine involving international experts. “This is a government with credibility and national acceptance,” Mulino said, highlighting his administration’s intention to begin addressing the mine’s future in early 2025.

Mulino has said the Cobre Panama project will be addressed as needed, but stressed that issues such as social security have higher priority. A clear timeline for this process, however, has yet to emerge.

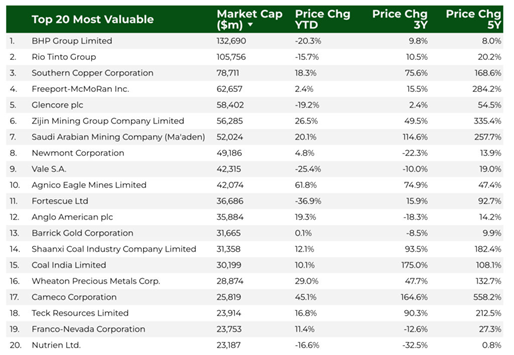

MINING.COM’s ranking of world’s 50 most valuable miners enjoyed a combined market capitalization of $1.51 trillion at the end of Q3, up by single digits since the start of the year compared to rip-roaring broader US and world markets.

Much of the drag on the index comes from the top – the mining industry’s traditional Big 5 – BHP, Rio Tinto, Glencore, Vale and Anglo American.

With the exception of Anglo, which received a fillip from BHP’s approach, the stocks are deep in the red for 2024.

Together, the large diversified companies have lost nearly $60 billion in value this year. One bad week – say copper retreats further and iron ore goes into double digits – would see them hit new 52-week lows. As the table shows, on a longer horizon their underperformance is even more startling.

In the past these stocks would consistently occupy the top five slots in the ranking, supported by vast asset portfolios covering a range of commodities across many regions.

In a boom and bust industry that was the key to success (if not survival) for companies that trace roots back many decades if not more than a century.

Donald Trump has described the Inflation Reduction Act (IRA) as a “green scam” and vowed to repeal it after he returns to the White House in January.

This is bad news for sectors such as electric vehicles (EV) and wind power, which have been major recipients of the Biden administration’s signature $369 billion energy transition legislation.

But some of the “new green deal” money has also been channeled to the US industrial base, such as the $75 million allocated for an upgrade of Constellium’s aluminum rolling mill in West Virginia.

Will this too be clawed back? It seems unlikely because when it comes to rebuilding US industrial capacity and cutting the country’s critical minerals dependency on China, there is remarkable cross-party consensus.

Congo’s Gecamines offers $1 million to block Chinese deal with Chemaf

The Democratic Republic of Congo’s state miner Gecamines is offering $1 million to buy cobalt and copper assets of indebted mining firm Chemaf to prevent China from increasing its control of critical metals in the country, two sources familiar with the details told Reuters.

Chemaf, a partner of commodities trader Trafigura, agreed to sell its copper and cobalt assets to Chinese defence and industrial giant, China North Industries Corp, or Norinco, in June.

Gecamines, which owns the lease to Chemaf’s mines, whose copper and cobalt are used in electric vehicles and clean energy infrastructure, was asked by Chemaf to approve the sale, but declined.

Gecamines later submitted an unsolicited bid for the Chemaf assets, deepening a standoff that has been complicated by US officials lobbying against China’s grip on the mineral-rich central African Copperbelt.

Chinese companies are major investors in Congo’s mining sector. CMOC Group is now the world’s biggest cobalt miner as it boosts output at Tenke Fungurume mine it bought from US-based Freeport-McMoRan just four years ago.

Scandinavian junior Akobo Minerals (FRA: 643) (OTCMKTS: AKOBF) officially opened on Wednesday its Segele gold mine in Ethiopia, marking a major milestone in the country’s developing mining industry.

The inauguration ceremony was attended by Ethiopia’s Prime Minister Abiy Ahmed, which shows the mine’s significance to the nation’s economic and industrial ambitions, Akobo said.

“The Segele mine is a testament to Ethiopia’s vast potential in the mining sector and the importance of international partnerships to realize this potential,” Ahmed said in the statement. “We are proud to see this project reach a significant milestone, benefiting not only the national economy but also the communities around it.”

The ceremony also included the first symbolic gold pour, with an initial yield of 6.5 kilograms, which the company says underscores Segele’s high-grade ore quality.

It follows Akobo’s October announcement of its first gold bar production from the site — a 1.4-kg bar smelted from 170 tonnes of lower-grade material, with an average grade of 8 grams per tonne.

Adani’s Australian coal unit faces human rights complaint

Part of the Doongmabulla Springs Complex.

India’s Adani Group, whose billionaire chairman has been indicted for fraud by US prosecutors, is facing accusations of racism at its Australian coal unit after an Aboriginal group filed a complaint with the country’s Human Rights Commission.

The Nagana Yarrbayn Wangan & Jagalingou Cultural Custodians in Queensland state said it filed a complaint alleging serious racial discrimination by the unit, Bravus Mining and Resources, earlier this week.

The complaint details how Adani employees sought to “verbally and physically obstruct and prevent” members of the Aboriginal group from accessing springs near Adani’s Carmichael coal mine “in order to perform cultural rites and share cultural knowledge”, the group said in a statement.

“We have endured years of discrimination and vilification from Adani, and we’re not putting up with this anymore,” Nagana Yarrbayn Senior Cultural Custodian, Adrian Burragubba said in the statement.

“Adani has been on notice about their conduct since our lawyers sent a concerns notice last year, and they refused to take action. Legal recourse is the only answer,” he added.

A Bravus spokesperson “wholly rejected” the group’s allegations, saying it was an attempt to stop Bravus from telling its side of the story and “sharing facts with the public about our interactions with him and members of his ‘Family Council’.”

It said the mine had been operating safely and responsibly in line with Queensland and Australian law and in partnership with the majority Traditional Owner group for the mining area under the terms of ratified Indigenous Land Use Agreements and Cultural Heritage Management Plans for more than two years.